Nailing Business Loan Eligibility: A No-Stress Guide

Securing financing for your business is often essential to fuel growth, expand operations, purchase new equipment, or manage everyday expenses. However, the process of qualifying for a business loan can seem confusing. It’s more than just submitting an application – it’s about knowing what lenders are looking for and how to make your business an attractive candidate for financing.

This guide will walk you through the main factors that lenders consider when determining eligibility for a business loan. Whether you’re a new entrepreneur or a seasoned business owner, you’ll learn how to improve your chances of getting the funding you need.

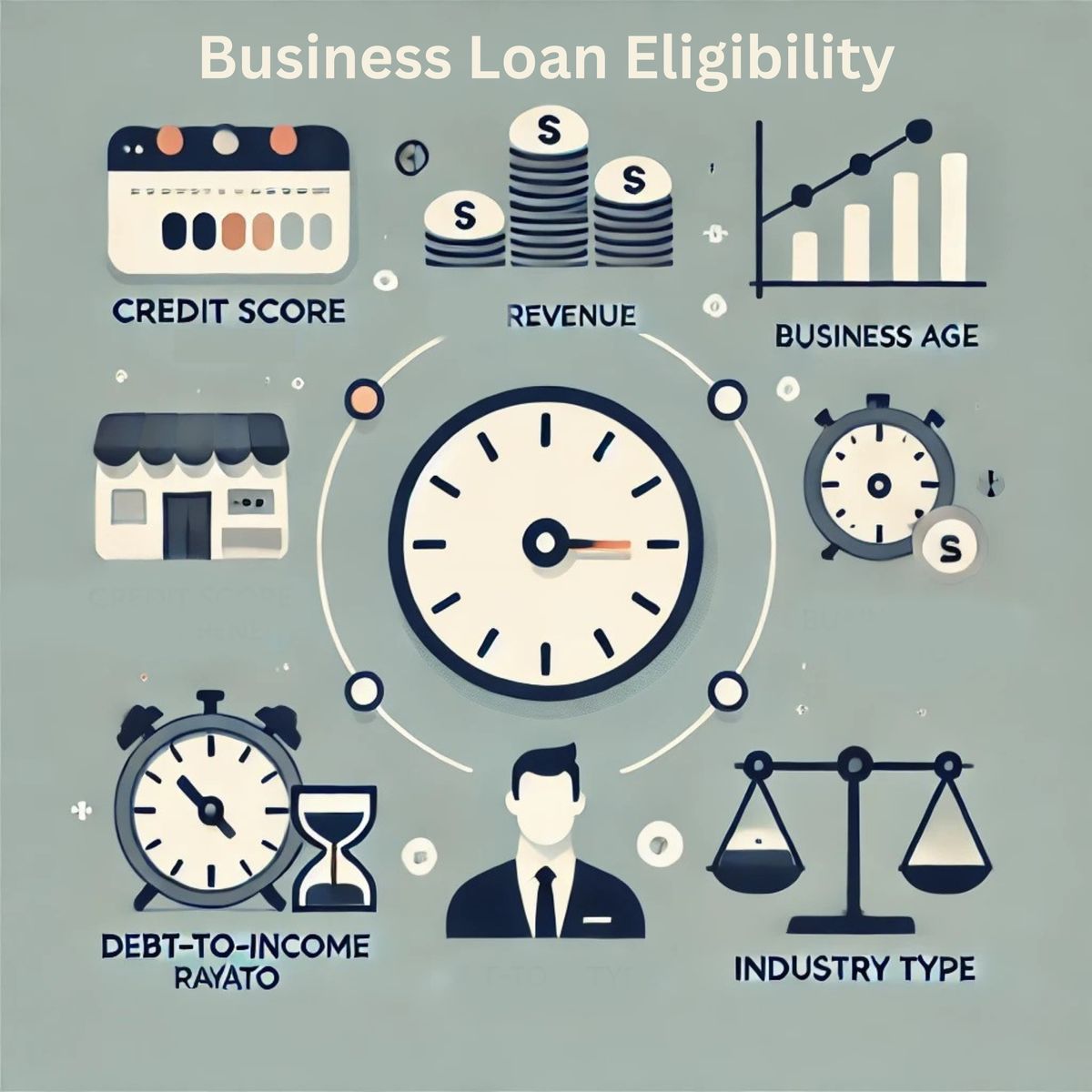

What Lenders Look For in Business Loan Applications

Getting a business loan isn’t as hard as it might seem, but lenders do have specific things they look for when deciding whether to approve your loan. Think of it like applying for a job—you need to show that you're the right fit. Let’s break down the key factors lenders consider, and we’ll throw in some easy examples along the way to make it crystal clear!

- Credit Score: Your Financial Report Card

Your credit score is one of the first things a lender checks. It’s like a report card that shows how well you’ve handled money in the past. This score reflects both your personal and business finances. A high score means you’ve been responsible—paying bills on time, managing debt well—so lenders feel more confident that you'll repay their loan.

Example: Let’s say you run a small bakery. If you’ve always paid your bills on time and have low credit card debt, your credit score will be high. This makes a lender more likely to approve your loan request to buy a new oven for ₹2 lakhs :)

- Annual Revenue: Show Me the Money!

Lenders want to see that your business is making money—enough money to cover loan payments without putting you in a tight spot. Your annual revenue shows how much money your business brings in over a year. The higher your revenue, the better your chances of getting approved.

Example: Imagine you own a landscaping business that makes ₹12 lakhs a year. You’re asking for a loan of ₹2 lakhs to buy new equipment. Since your revenue is much higher than what you’re borrowing, the lender feels reassured that you can handle the loan payments.

- Business Age: Stability Matters

Lenders usually prefer businesses that have been around for a while—typically at least two years. This tells them that your business is stable and more likely to succeed in the long run. If your business is newer, they’ll still consider you, but they might focus more on your business model and potential for growth.

Example: You run an e-commerce shop that’s been doing well for four years. Lenders will see your business as stable because you’ve already survived the tough early years. This makes them more willing to lend you ₹5 lakhs compared to a brand-new startup.

- Profitability: It’s Not Just About Sales

Having a high revenue is great, but it’s not the whole picture. Lenders also look at how much of that money is left after paying all your expenses (rent, salaries, materials, etc.). This is your profit. A profitable business shows that you have extra cash to cover loan payments, making you a safer bet.

Example: Let’s say your annual revenue is ₹16 lakhs, but after paying all your expenses, your profit is only ₹80,000. A lender might be cautious because you don’t have a lot of wiggle room for extra costs, like loan payments.

- Industry Type: Risky or Reliable?

Some industries are considered riskier than others. For example, restaurants and construction businesses may have a higher chance of failure due to market fluctuations, seasonality, or competition. If you’re in a riskier industry, lenders may look more closely at your business plan or require more collateral.

Example:You own a small tech consulting firm in a stable industry with steady clients. Lenders see this as a safe investment compared to someone opening a brand-new restaurant, which can be more unpredictable.

- Debt-to-Income Ratio: Keeping Debt Under Control

Your debt-to-income ratio tells lenders how much of your income is already going toward paying off debts. A lower ratio means you aren’t drowning in debt, which makes lenders more likely to trust that you can handle another loan. It’s like a balance—too much debt, and you’re seen as a risk.

Example: Let’s say your business earns ₹8 lakhs a year, but you’re already paying ₹1.6 lakhs annually to pay off another loan. That’s a 20% debt-to-income ratio, which is pretty reasonable. But if you were paying ₹4 lakhs in debt, that’s 50%—a much higher risk for lenders.

Bringing It All Together

Imagine you own a bakery that’s been in business for three years. You’re looking for a ₹25 lakh loan to buy new equipment and expand your shop. Here’s how your situation stacks up:

- Credit Score: You’ve always paid bills on time and have low debt, so your credit score is excellent.

- Annual Revenue: Your bakery brings in ₹20 lakhs a year, so lenders see that you have a healthy income.

- Business Age: Three years in business shows that you’re established and stable.

- Profitability: After expenses, you’re left with a solid profit of ₹5 lakhs, proving you have room to make loan payments.

- Industry Type: While the food industry can be competitive, your long-standing presence and loyal customer base put you in a safer position.

- Debt-to-Income Ratio: You have minimal debt, with a low debt-to-income ratio, making lenders feel more secure in offering you a loan.

In this scenario, you’re likely to get approved because you check off all the boxes lenders care about.

Conclusion

Getting a business loan in India is easier when you understand what lenders are looking for. Focus on building a strong credit score, maintaining healthy revenue and profitability, and keeping debt under control. With this knowledge, you’ll be better prepared to navigate the loan process and secure the funding you need to grow your business.

So, whether you’re applying for a loan from any financial institution, being well-prepared will boost your chances of approval and help you secure the right loan for your business.